Social Sentiment from SMA (Alternative Data) - Making a losing strategy profitable

td753764

Posts: 67

td753764

Posts: 67

Hi All,

Over the past months, I have spent some time working on our alternative data. There is a lot more to come soon.

However, I did take some time to put together a backtest that shows some of the power of this alternative data.

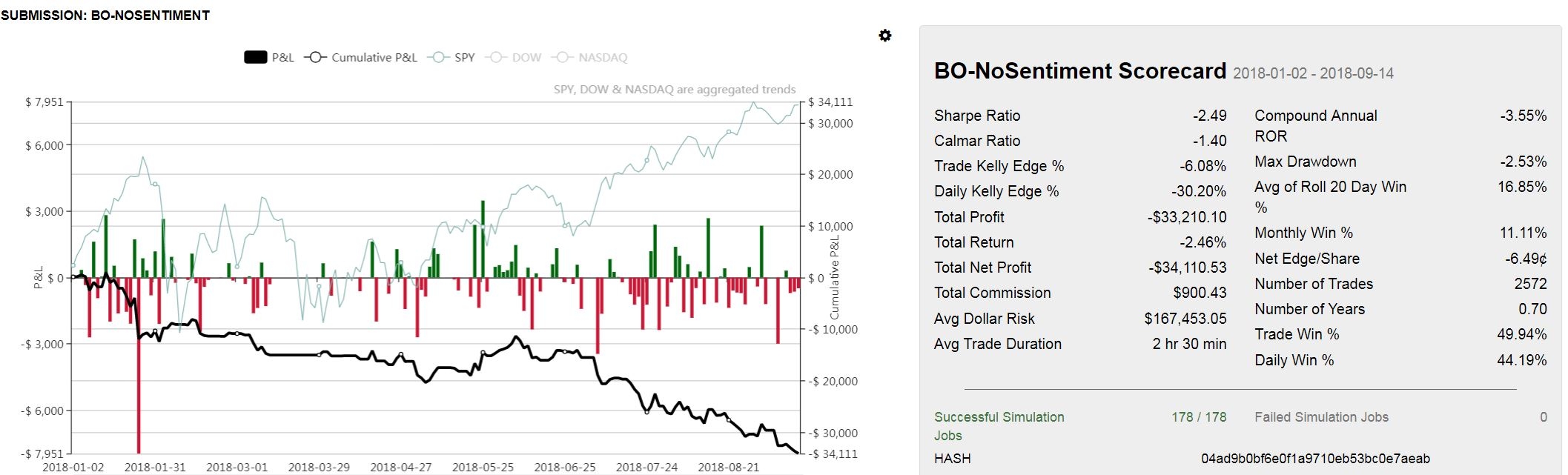

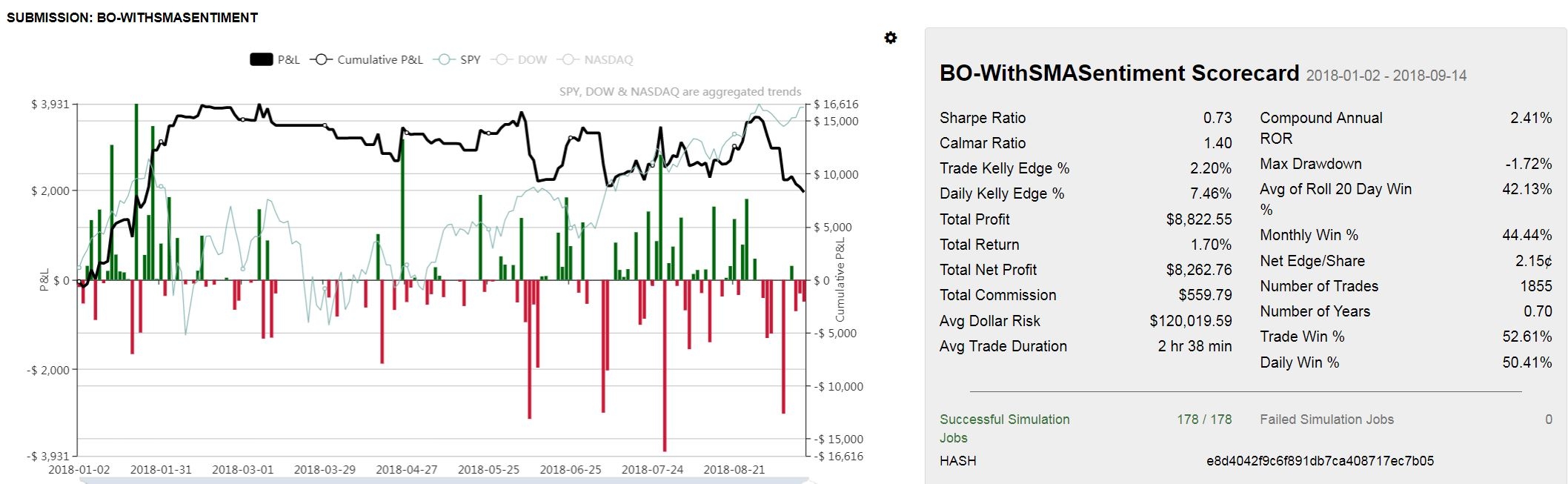

Alternative datasets are improving our trading strategies at CloudQuant. In the following example, we added an easy check of social sentiment. Before going long, check to see if social sentiment was favorable. Instead of following the original algo, simply add this additional check. If sentiment was positive, go ahead and go long. Otherwise, don’t trade. This social sentiment provided an insurance policy essentially for the underlying strategy, and it improves the performance. One can easily see the results in the following diagrams where the first trading strategy lost money and the second made over $170,000.

Original Breakout Strategy Without Alternative Data

Same Script - Adding in Check for SMA Alternative Data

Comments

--- Note -- This script works for CQ Elite...

to request upgrade to elite use: https://forum.cloudquant.com/discussion/206/upgrading-to-cq-elite#latest

Source Code to the script with the SMA Sentiment

Hi mr

How can I get your database?

This dataset is now only available as a paid dataset from https://catalog.cloudquant.com