Read a file for symbols that are in your own private file to only process your own symbols.

Hi All,

I was recently asked a question on how does someone read a file with a private list of symbols.

Step 1. Create your own file in the User Data tab.

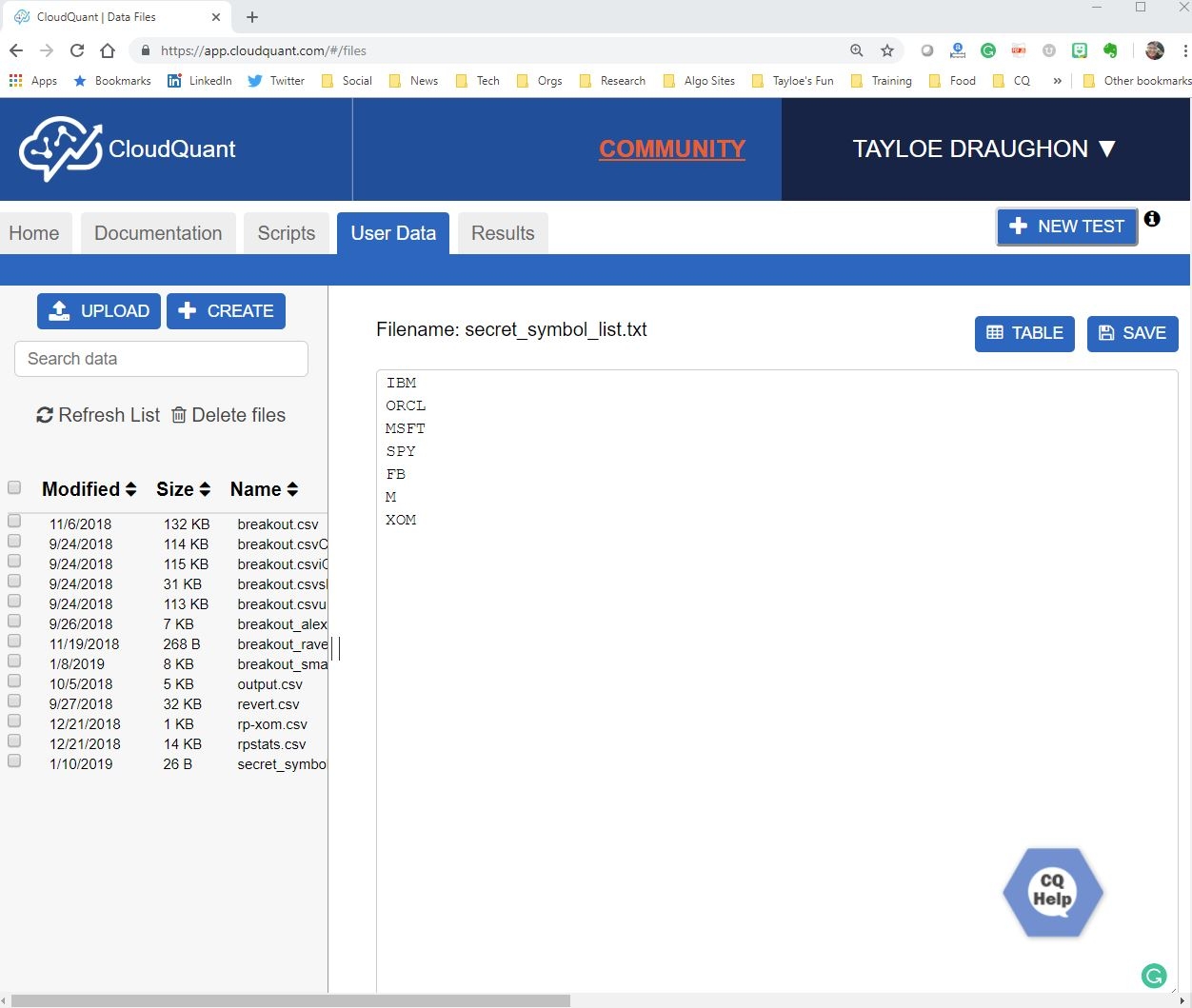

I created a file that has my list of symbols. The file is called "secret_symbol_list.txt"

Each row of the file has a different symbol. Here is my "secret_symbol_list.txt"

IBM

ORCL

MSFT

SPY

FB

M

XOM

For those unfamiliar with the CloudQuant User Data Tab, this is what it looks like:

Step 2. Read the file in on_strategy_start

Not every algo has an on_strategy_start() method. I use this method to load up the symbols into a class list variable so that it is available to all instances as my algo runs.

@classmethod

def on_strategy_start(cls, md, service, account):

# read the user data file as a string

cls.symbol_list = []

symbols = service.read_file('secret_symbol_list.txt', format='raw')

# create a symbol list by splitting the lines into a list of symbols

cls.symbol_list = symbols.splitlines()

Step 3. Return True in is_symbol_qualified if the symbol is in your list

The is_symbol_qualified method lets the backtest simulation engine know if we are using this symbol for trading.

@classmethod

def is_symbol_qualified(cls, symbol, md, service, account):

# qualify only symbol in both the symbol list and in the entry stats file

if symbol in cls.symbol_list:

print("This symbol {} is in my list.".format(symbol))

return True

Full Working Script that uses this technique

from cloudquant.interfaces import Strategy

import talib

import numpy

#####################################################

# Simple Exponential Moving Average Script

# When yesterday's EMA is above the previous day's EMA

# then go long - else go short

class Simple_EMA(Strategy):

@classmethod

def on_strategy_start(cls, md, service, account):

# read the user data file as a string

cls.symbol_list = []

symbols = service.read_file('secret_symbol_list.txt', format='raw')

# create a symbol list by splitting the lines into a list of symbols

cls.symbol_list = symbols.splitlines()

@classmethod

def is_symbol_qualified(cls, symbol, md, service, account):

# qualify only symbol in both the symbol list and in the entry stats file

if symbol in cls.symbol_list:

print("This symbol {} is in my list.".format(symbol))

return True

def on_start(self, md, order, service, account): #

myBars = md.bar.daily(start=-21) # grab 21 bars, EMA uses 20, we want yesterdays and the day before so grab 21

close = myBars.close # pull out just the close prices

EMA = talib.MA(close,timeperiod=20,matype=1) # TALIB Moving Average matype=1 = Exponential Moving Average

EMAlist = numpy.ndarray.tolist(EMA) # TALIB returns a numpy array, lets turn that back into a basic list

#print self.symbol,EMAlist

if EMAlist[-1] > EMAlist[-2] : # if yesterday's EMA is above the previous day go long

order.send(self.symbol, 'buy', 100, type='MKT') # Market order, no price required

print("long entry ordered on {}".format(self.symbol))

if EMAlist[-1] < EMAlist[-2] : # if yesterday's EMA is below the previous day go short

order.send(self.symbol, 'sell', 100, type='MKT') # Market order, no price required

print("short entry ordered on {}".format(self.symbol))

def on_minute_bar(self, event, md, order, service, account, bar):

if event.timestamp > service.time(15,44): # at the end of the day, exit the position and terminate the script

if account[self.symbol].position.shares > 0:

order.send(self.symbol, 'sell', 100, type='MKT') # Market order, no price required

print("sell to cover ordered on {}".format(self.symbol))

elif account[self.symbol].position.shares < 0:

order.send(self.symbol, 'buy', 100, type='MKT') # Market order, no price required

print("buy to cover ordered on {}".format(self.symbol))

Tagged:

Comments

Also would be great to see a good example of working with files which contain list of trades. For example

AAPL,20180101 12:15:18.200,200,"buy","mkt"

AAPL,20180101 12:20:21.300,200,"sell","mkt"

AAPL,20180101 15:30:00.000,500,"buy","MOC"

Hi:

If you are using a CSV file, it is easier to have column headings.

For this example, I am going to use a file called signals.csv which contains the following data.

Reading in the data from my signals.csv file can be accomplished using the following line of code. The return of this will be a list containing dictionary data.

data = service.read_file('signals.csv', 'csv')To See what is in data you can print it out by iterating through the list.

This produces the following prints:

Because this is a list of dictionaries you can now reference each of the elements by name. For example:

Timestamps, datetime, MUTS - dealing with problems of converting your timestamp.

My data file has a representation of the timestamp that looks like: 20180710 12:15:18.200

To process this we may need to convert the timestamp string into a datetime field. code that I used for that process. The following code handles this logic for me.

Full Working Script - To Replay a Signal file.