Last Hour of the Day

Came across some info on the internet so I thought I would do a quick CloudQuant test...

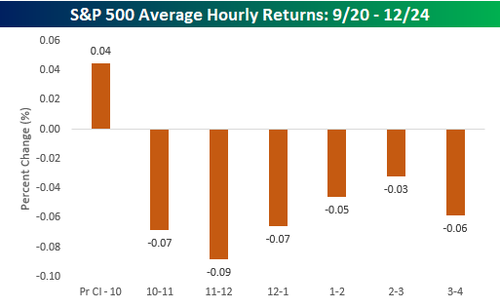

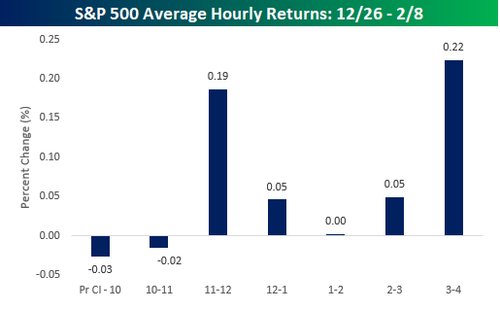

"Heading into Monday, the S&P 500 had been up in the final hour of trading for seven straight days, and over the prior five weeks, the last hour of trading saw positive returns 90% of the time! That kind of late day strength doesn’t occur all that often."

The script uses timers so is for CloudQuant Elite. Because return was positive from 10am the timer for entry triggers at 10am. The commented out line is still there so you can switch to Entry 1 hour before the close instead.

from cloudquant.interfaces import Strategy

class lev_to_for(Strategy):

@classmethod

def is_symbol_qualified(cls, symbol, md, service, account):

return symbol in ["SPY","XLY","XLF","XLK","XLV","XLB","XLE","XLV","XLP","XLI","XLRE"]

# return symbol in ["AMZN","FB","AAPL","GOOG","GOOGL","NFLX"]

# return symbol in ["SPY","XLY","XLF","XLK","XLV","XLB","XLE","XLV","XLP","XLI","XLRE","AMZN","FB","AAPL","GOOG","GOOGL","NFLX"]

def on_start(self, md, order, service, account):

service.clear_event_triggers()

closetime = md.market_close_time

# service.add_time_trigger(closetime-service.time_interval(1), timer_id = 'enter') # enter 1 hour before close

service.add_time_trigger(service.time(10), timer_id = 'enter') # enter at 10am

service.add_time_trigger(closetime-service.time_interval(0,15), timer_id = 'marketonclose')

def on_timer(self, event, md, order, service, account):

if event.timer_id == "enter":

mopen = md.L1.open

mlast = md.L1.last

mclose = md.stat.prev_close

mcltoop = (mopen-mclose)/mclose

moptola = (mlast-mopen)/mclose

mcltola = (mlast-mclose)/mclose

print "{} {:<6} close{:8.2f} open{:8.2f} last{:8.2f} open-close{:8.2f} {:8.2f}% last-open{:8.2f} {:8.2f}% last-close{:8.2f} {:8.2f}%".format(service.time_to_string(event.timestamp),self.symbol,mclose,mopen,mlast,mopen-mclose,mcltoop,mlast-mopen,moptola,mlast-mclose,mcltola)

mshares = int(10000/mclose)

order.send(self.symbol, 'buy', mshares, type='MKT') # simple market order

# order.vwap(self.symbol, mshares, "buy", time_frame=60, num_slices = 10, order_aggression=3) # VWAP order over 60 minutes in 10 slices

if event.timer_id == "marketonclose":

mshares=account[self.symbol].position.shares

print self.symbol,mshares

if mshares>0:

order.send(self.symbol, 'sell', mshares, type='MOC')

elif mshares<0:

order.send(self.symbol, 'buy', mshares, type='MOC')